How Much Does a $500,000 Surety Bond Cost?

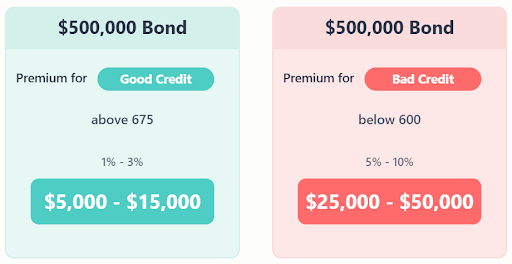

A $500,000 surety bond typically costs between $5,000 and $50,000 per year. This premium generally ranges from 1% to 10% of the total bond amount. Your specific cost depends on the bond type, your personal credit score, and your business's financial strength. Highly qualified applicants with robust financials usually secure rates on the lower end of this spectrum.

When you're told you need a half-million-dollar bond, the number can be intimidating. However, it’s a common misconception that you have to pay the full $500,000. In our experience, once business owners realize they are only paying a small percentage of that sum, the process becomes much more manageable.

That’s why we feel it’s important to be transparent about pricing. Whether you're bidding on a major project or meeting federal broker requirements, the price reflects the risk the surety takes for you. According to the Small Business Administration (SBA), surety bonds are vital for risk management, ensuring contracts are completed and subcontractors are paid. This guide breaks down exactly what goes into a $500,000 surety bond cost.

$500,000 Surety Bond Cost Overview

Surety bond premiums are calculated by multiplying the total bond amount by a rate determined during underwriting. It is vital to distinguish between the penal sum ($500,000)—the maximum claim amount—and the premium, which is your out-of-pocket cost. Rates can be structured as flat fees, tiered scales, or deviated rates depending on the specific industry and risk category.

Surety companies use several rate structures. For standard license bonds, you might see standard rates based on credit. For larger contract bonds, sureties often use sliding scales, where the rate decreases as the bond amount increases.

Here at Lance Surety, we know that understanding these tiers is key to budgeting. Class rates are set for specific industries, while account rates are negotiated for high-volume businesses. If you have an established relationship with a surety, you may qualify for deviated rates, which are lower than standard filed prices.

Surety bond cost calculator

Common Types of $500,000 Surety Bonds

Bonds at this level are common in heavy industry, large-scale construction, and high-stakes financial services. The most frequent requests involve contract-related performance bonds and high-limit commercial licenses for mortgage lenders or money transmitters. Each bond type carries a distinct risk profile, which directly influences the premium rate assigned by the underwriter during the review.

Contract and Performance Bonds

These are most common in construction. Performance bonds guarantee project completion, while payment bonds ensure laborers and suppliers are paid. When securing a facility for a $500,000 project, you may also encounter bid bonds and annual administration fees. In our experience, design-build projects often carry a surcharge because they involve more complex liability than standard build-only contracts.

License, Permit, and Other Bond Types

This category includes money transmitter bonds and ERISA fidelity bonds. Some states require $500,000 mortgage lender bonds to protect consumers. Court bonds, such as appeal or supersedeas bonds, are also frequently set at this amount. Because these often have higher claim rates than local licenses, the underwriting is generally more rigorous.

What Affects the Cost of a $500,000 Surety Bond?

The primary drivers of your bond premium are your personal credit and your business's financial health. Underwriters look for high net worth, strong working capital, and a clean claims history. Conversely, past bankruptcies, weak financial statements, or high industry-wide claim rates will push the premium toward the higher end of the 1% to 10% range.

Your credit score is significant for instant-issue bonds, but at the $500,000 level, working capital—your current assets minus liabilities—is king. Sureties want to see that you can handle a business hiccup without triggering a claim. As noted by the National Association of Surety Bond Producers (NASBP), the surety is looking for evidence of the three C’s: Character, Capacity, and Capital.

Underwriting a High-Value Bond

For a $500,000 bond, sureties move beyond a simple credit check to full underwriting. This involves a comprehensive review of your balance sheet, profit and loss statements, and business history. The underwriter assesses your revenue and previous project history to ensure you have the capacity to manage the obligations associated with a high-value bond.

Here at Lance Surety, we know this stage can feel invasive, but it’s standard for high-limit bonds. The underwriter may set financial covenants or bond facility limits—essentially a credit limit for your active bonds. For very risky bonds, you might be asked for collateral, though this is rare for businesses with strong financial statements.

How to Lower Your $500,000 Bond Premium

Securing a lower rate is often a matter of proactive financial management. You can reduce your premium by improving your credit score, paying down debt, and building your business's net worth. Additionally, working with a specialized surety broker provides access to deviated rates and multi-year discounts that general insurance agents typically cannot offer.

In our experience, providing CPA-reviewed or audited financial statements rather than internal reports often results in a lower rate. This gives the surety more confidence in your numbers. Building a clean bonding history—meaning no claims filed against you over several years—is also a major factor in securing preferred pricing.

Getting a $500,000 Bond with Bad Credit

While poor credit or thin financial history makes bonding more expensive, it rarely makes it impossible. Specialized programs for bad credit surety bonds exist to help entrepreneurs stay in business. In these cases, expect premiums between 1% and 5%, and be prepared to provide additional documentation regarding your project history and professional record.

We know a low credit score doesn't define a business owner. That’s why we feel it’s important to work with a broker who understands the non-standard market. Most applicants with credit issues still qualify if they don't have open bankruptcies. You can often start the process with a simple online application to see your options.

Premium Financing and Payment Options

Large premiums don't always have to be paid in one lump sum. Many surety agencies offer financing plans that allow you to pay in monthly installments. This is particularly helpful for $500,000 bonds where the premium might exceed $15,000, as it preserves your business's cash flow for essential daily operations.

Your bond specialist can arrange these options based on your financial needs. For standard bonds, we offer a secure online checkout. For larger $500,000 bonds, we typically handle the payment arrangements directly to ensure the financing terms align with your business goals and the surety's requirements.

Where to Get Your $500,000 Surety Bond

Purchasing a high-value bond requires an agency with direct access to T-listed, A-rated bonding companies. A specialized broker like Lance Surety understands full underwriting and can help you navigate programs like the SBA Surety Bond Guarantee Program, which assists small businesses in securing bonds they might not otherwise qualify for.

Don't settle for a general agent with limited market access. A broker focused on surety has the expertise to shop your file to multiple carriers for the best rate. When you're ready, you can fill out our online application to get the process moving quickly.

Frequently Asked Questions

Is a $500,000 surety bond premium refundable?

Generally, premiums are earned once the bond is issued. However, if a bond is canceled or a contract reduced shortly after issuance, you may be eligible for a prorated refund, depending on the surety’s specific terms.

How long does it take to get a $500,000 surety bond?

Full underwriting typically takes 3 to 5 business days once all financials are submitted. While credit-based bonds are faster, high-limit bonds require the surety to do thorough due diligence.

Can I get a $500,000 bond with no prior bonding history?

Yes. Underwriters will rely heavily on your current financial statements, personal net worth, and industry experience. If you prove you have the Capital and Capacity, a long history is less critical.

Do I pay the full $500,000?

No. You only pay the premium, a small percentage of that amount. The $500,000 is the guarantee to your obligee. To find your rate, check our resources on surety bond cost.

Sources

Arizona Court of Appeals, Division One. (n.d.). What to know about supersedeas bonds. https://coa1.azcourts.gov/Portals/1/What%20to%20Know%20About%20Supersedeas%20Bonds.pdf

Congressional Research Service. (2025, July 18). SBA surety bond guarantee program (CRS Report No. R42037).

https://www.congress.gov/crs-product/R42037

Federal Motor Carrier Safety Administration. (n.d.). Broker and freight forwarder financial responsibility rule: Overview and compliance. U.S. Department of Transportation.

https://www.fmcsa.dot.gov/registration/broker-and-freight-forwarder-financial-responsibility-rule-overview-and-compliance

Lance Surety Bonds. (n.d.-a). Bad credit surety bonds.

https://www.lancesuretybonds.com/learn/bad-credit-surety-bonds

Lance Surety Bonds. (n.d.-b). Performance bonds.

https://www.lancesuretybonds.com/contract-bonds/performance-bonds

Lance Surety Bonds. (n.d.-c). Surety bond cost.

https://www.lancesuretybonds.com/learn/surety-bond-cost

Lance Surety Bonds. (n.d.-d). Surety bond quote.

https://www.lancesuretybonds.com/surety-bond-quote

National Association of Surety Bond Producers. (n.d.). National Association of Surety Bond Producers.

https://www.nasbp.org/

National Association of Surety Bond Producers. (2021). Surety prequalification goes beyond the three Cs. Surety Bond Quarterly, Winter 2021.

https://www.nasbp.org/wp-content/uploads/2024/11/Surety_Prequalification_Goes_Beyond_Three_Cs_-_SBQ_Winter_2021.pdf

U.S. Department of Labor, Employee Benefits Security Administration. (n.d.). Protect your employee benefit plan with an ERISA fidelity bond.

https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/publications/erisa-fidelity-bond.pdf

U.S. Department of the Treasury, Bureau of the Fiscal Service. (n.d.). Surety bonds.

https://fiscal.treasury.gov/about-us/doing-business-with-fiscal-service/surety-bonds

U.S. Small Business Administration. (n.d.-a). Surety bonds.

https://www.sba.gov/funding-programs/surety-bonds

U.S. Small Business Administration. (n.d.-b). U.S. Small Business Administration.

https://www.sba.gov/

Latest posts by JD Weisbrot (see all)

- - Jul 02, 2026

- - Jul 02, 2026

- - Jul 02, 2026

Get a FREE Surety Bond Quote in Minutes

-

Fast and Secure Application

Fast and Secure Application -

Money Back Guarantee

Money Back Guarantee -

Approval in Minutes

Approval in Minutes -

Nationwide Coverage

Nationwide Coverage

Recommended Articles

-

Fast and Secure Application

Fast and Secure Application -

Nationwide Coverage

Nationwide Coverage -

Approval in Minutes

Approval in Minutes -

Money Back Guarantee

Money Back Guarantee

- Image

- Image

- Image

Lance Surety Bond Associates, Inc. is a surety bond agency based out of southeastern Pennsylvania that is able to write all surety bond types in all 50 states. We are dedicated to servicing all of our customers' surety bonding needs throughout the country and guarantee competitive rates, timely responses, and unparalleled customer service.